Global Food Intolerance Products Market Report | Market Size, Industry Analysis, Growth Opportunities, & Forecast (2025-2030)

Global Food Intolerance Products Market Overview

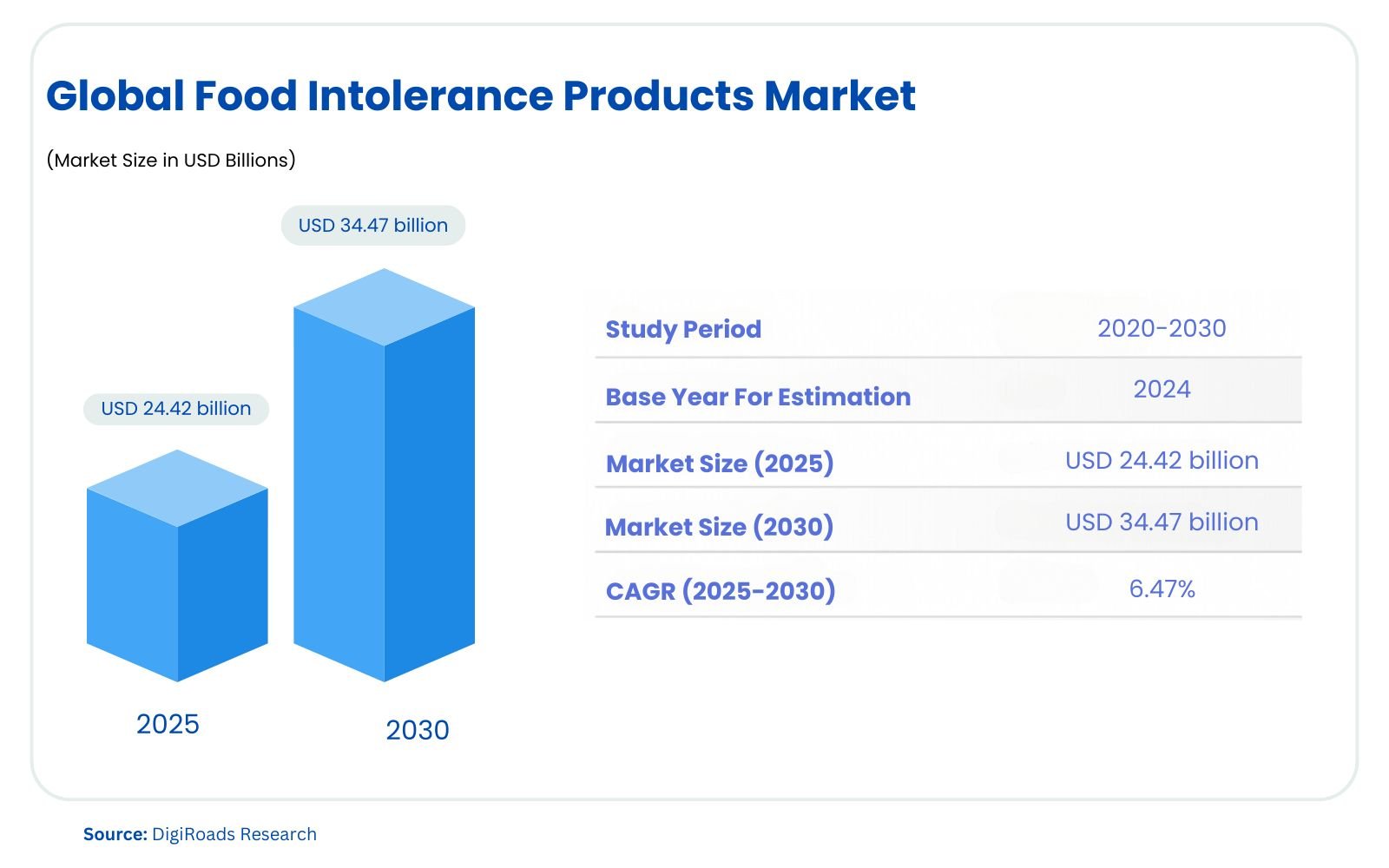

The global food intolerance products market is witnessing steady growth, with an estimated market size of USD 24.42 billion in 2025, and is projected to reach USD 34.47 billion by 2030, expanding at a CAGR of 6.47% during the forecast period 2025-2030. The global food intolerance products market is expected to witness significant growth from 2025 to 2030, driven by rising consumer demand for specialized dietary options and increased awareness of food intolerances such as gluten and lactose sensitivity. As consumers become more health-conscious, the demand for clean-label, gluten-free, lactose-free, and plant-based products continues to rise. This market encompasses a diverse range of product categories, including bakery products, confectionery items, dairy and dairy alternatives, sauces, and condiments.

The food intolerance products market is segmented based on product types, labeling claims, distribution channels, and geographic regions. Key segments include gluten-free and lactose-free foods, with distribution channels such as supermarkets, online retail, and convenience stores playing a vital role in market expansion. North America currently holds the largest market share, while Asia-Pacific is expected to grow at the highest rate during the forecast period.

Leading players such as General Mills, Danone, Beyond Meat, Nestlé, and Reckitt Benckiser are enhancing their product portfolios to cater to the growing demand for food intolerance products. With increasing product innovation and a shift towards healthier diets, the market is set to continue its upward trajectory from 2025 to 2030.

Market Report Coverage:

The “Global Food Intolerance Products Market Report—Future (2025-2030)” by Digiroads Research & Consulting covers an in-depth analysis of the following segments in the market.

| Product Type | Bakery Products, Confectionery Products, Dairy and Dairy Alternatives, Meat and Seafood, Sauces, Condiments and Dressings, Other Product Types |

| Distribution Channel | Supermarkets/Hypermarkets, Convenience/Grocery Stores, Online Retail Stores, Other Distribution Channels |

| Geography | North America (United States, Canada, Mexico, Rest of North America), Europe (Spain, United Kingdom, Germany, France, Italy, Russia, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, Rest of Asia-Pacific), South America (Brazil, Argentina, Rest of South America), Middle East and Africa (South Africa, United Arab Emirates, Rest of Middle East and Africa) |

Study Assumptions and Definitions

The study on the global food intolerance products market is based on several key assumptions and precise definitions to ensure comprehensive analysis and accurate market insights.

Food intolerance products refer to specialized food items designed to cater to individuals with dietary restrictions or sensitivities. These include products labeled as gluten-free, lactose-free, or plant-based, aimed at addressing specific health concerns and improving overall dietary choices. The study assumes steady growth in consumer awareness about food intolerances, increased adoption of healthy lifestyles, and rising demand for clean-label and allergen-free products.

Market estimations consider a combination of primary and secondary research, ensuring accuracy and reliability. Key factors like evolving dietary preferences, regulatory frameworks, and innovations in food production are also incorporated. The market forecast for 2025-2030 is calculated based on historical trends, current dynamics, and potential future developments, with a focus on segment-wise and region-wise performance.

Geographical segmentation assumes varying growth trajectories, driven by economic conditions, demographic patterns, and cultural dietary habits. For instance, North America leads due to high awareness levels, while the Asia-Pacific region is expected to grow significantly due to urbanization and increased consumer spending.

This study adopts a holistic approach, ensuring all assumptions and definitions align with industry standards and market dynamics.

Market Scope

The global food intolerance products market focuses on catering to individuals with specific dietary needs or sensitivities, including lactose intolerance, gluten intolerance, and other dietary preferences. This market encompasses a diverse range of product types such as bakery items, confectionery products, dairy and dairy alternatives, meat and seafood, sauces, condiments, and dressings.

The analysis covers distribution channels, including supermarkets/hypermarkets, convenience/grocery stores, online retail platforms, and others, providing insight into consumer purchasing behaviors. The geographical scope spans key regions like North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, offering a detailed understanding of regional market dynamics.

The study examines market trends, innovations, and competitive landscapes, focusing on drivers such as growing health awareness, demand for clean-label products, and evolving dietary habits. With a forecast period from 2025 to 2030, the report provides valuable insights for stakeholders, aiding in strategic decision-making and identifying growth opportunities.

MARKET OUTLOOK

Executive Summary

The global food intolerance products market is poised for significant growth from 2025 to 2030, driven by rising consumer awareness and demand for specialized dietary solutions. As health consciousness increases globally, consumers are seeking clean-label, allergen-free, and nutritionally superior food products. This market includes a diverse range of products such as bakery goods, confectionery, dairy and dairy alternatives, meat and seafood, and sauces, condiments, and dressings.

North America leads the market, fueled by high health awareness, advanced retail infrastructure, and growing lactose and gluten intolerance cases. For instance, approximately 36% of the U.S. population reportedly suffers from lactose intolerance, boosting demand for dairy-free and lactose-free alternatives. Europe and Asia-Pacific are also experiencing robust growth, with Asia-Pacific projected to achieve the highest CAGR, driven by urbanization, lifestyle changes, and growing middle-class populations.

The market is highly competitive, featuring major players like Danone SA, Nestlé SA, General Mills Inc., Reckitt Benckiser Group Plc, and Beyond Meat. These companies focus on product innovation, expansion, and partnerships to strengthen their market positions. Recent launches, such as plant-based alternatives and clean-label products, exemplify the industry’s dynamic nature. For example, Califia Farms introduced organic almond and oat milk in 2023, catering to the demand for simple, nutritious ingredients.

Despite its promising outlook, the market faces challenges like high production costs and stringent regulatory requirements. However, growing investment in research and development and the increasing availability of products through online retail channels present significant opportunities for growth.

The report offers comprehensive insights into market dynamics, segmentation, competitive landscapes, and future trends, serving as a valuable resource for industry stakeholders to make informed strategic decisions. With a projected CAGR of 6.47%, the food intolerance products market is set to witness sustained growth and innovation in the coming years.

COMPETITIVE LANDSCAPE

The Global Food Intolerance Products Market is moderately fragmented, with regional and multinational players competing fiercely for market share.

Key Market Players

- General Mills Inc.

- Danone SA

- Beyond Meat

- Nestlé SA

- Reckitt Benckiser Group PLC

- Blue Diamond Growers

- Abbott Laboratories

- The Kellogg Company

- Oatly Group AB

- Dr. Schär AG/SPA

Market Share Analysis

The global food intolerance products market is characterized by intense competition, with several key players holding significant market shares. Companies such as General Mills Inc., Danone SA, Beyond Meat, Nestlé SA, and Reckitt Benckiser Group PLC dominate the market due to their strong brand presence, extensive product portfolios, and robust distribution networks. These players invest heavily in research and development to introduce innovative products catering to diverse consumer preferences, including gluten-free, lactose-free, and vegan options.

The market is highly fragmented, with regional and local players contributing to its dynamic nature. In North America, established brands leverage consumer health awareness to maintain a competitive edge, while in the Asia-Pacific region, emerging players capitalize on growing demand for plant-based and free-from products.

Strategic initiatives such as mergers, acquisitions, partnerships, and product launches play a crucial role in maintaining market shares. For instance, Beyond Meat’s collaboration with global distributors and Danone’s expansion of plant-based dairy alternatives have strengthened their positions. Additionally, increasing e-commerce penetration has allowed smaller players to access a broader consumer base.

The evolving consumer focus on clean-label and sustainable products continues to drive competition, with market players striving to capture greater market share through innovation and adaptability.

MARKET DYNAMICS

Market Drivers and Key Innovations

The global food intolerance products market is driven by increasing consumer awareness regarding health and wellness, alongside a rising prevalence of food intolerances such as gluten and lactose sensitivities. Growing demand for clean-label and sustainable food products has propelled the adoption of specialized dietary options, including gluten-free, lactose-free, and vegan alternatives. This shift is further supported by heightened consumer focus on the benefits of plant-based diets and the environmental impact of food production.

Health-conscious consumers are increasingly prioritizing functional foods that promote better digestion, immune system support, and overall well-being. For instance, lactose-free products are perceived as aiding in weight management and reducing digestive discomfort, while gluten-free alternatives cater to those with celiac disease or gluten sensitivity.

Key innovations within the industry include the development of plant-based and allergen-free products, enhanced by advancements in food technology. Companies like Beyond Meat and Danone SA are leveraging novel processing techniques to create dairy and meat alternatives with improved texture, flavor, and nutritional profiles. For example, Danone’s Nextmilk mimics traditional dairy products while being completely plant-based.

Furthermore, product launches with simplified ingredient lists and fortified nutritional content are meeting the demand for clean-label offerings. Companies are also utilizing eco-friendly packaging to appeal to environmentally conscious consumers. Strategic collaborations, such as Beyond Meat’s partnerships to expand its market footprint, highlight the industry’s commitment to innovation and sustainability.

Overall, the market is poised for growth as key drivers and innovations align with evolving consumer preferences, fueling demand for diverse, health-centric food intolerance solutions.

Market Challenges

- High Manufacturing Costs: Producing food intolerance products involves specialized processes and ingredients, leading to elevated production costs, which may limit affordability for consumers.

- Regulatory Compliance: Strict regulations and certifications for gluten-free, lactose-free, and vegan labeling increase the complexity and cost of market entry for new players.

- Limited Consumer Awareness in Emerging Markets: In regions with low awareness of food intolerances, consumer demand for specialized products remains subdued, impacting market growth.

- Taste and Texture Challenges: Achieving the desired taste and texture in plant-based and allergen-free products can be challenging, reducing consumer satisfaction and repeat purchases.

- Competition from Conventional Products: Traditional food products often dominate due to their established market presence and lower cost, creating stiff competition for food intolerance alternatives.

- Supply Chain Constraints: Sourcing high-quality allergen-free ingredients and ensuring contamination-free supply chains present logistical challenges for manufacturers.

- Short Shelf Life: Many food intolerance products, particularly those free from preservatives, have a shorter shelf life, complicating storage and distribution logistics.

- Market Fragmentation: The presence of numerous regional and local players leads to intense competition, making it difficult for companies to capture significant market share.

- Consumer Misconceptions: Misunderstanding about the need for food intolerance products among individuals without diagnosed intolerances can deter market expansion.

- Economic Uncertainty: Fluctuating economic conditions may affect consumer spending on premium, health-focused food products.

Market Opportunities

- Growing Health Consciousness: As more consumers prioritize health and wellness, there is an increasing demand for food intolerance products such as gluten-free, lactose-free, and plant-based alternatives.

- Rising Prevalence of Food Intolerances: The increasing number of individuals diagnosed with food intolerances (e.g., lactose intolerance, gluten sensitivity) presents a substantial market opportunity for specialized products.

- Expanding Vegan and Plant-based Trends: The growing trend of veganism and plant-based diets is a significant opportunity for companies to introduce new dairy-free, meat-free, and allergen-free products.

- Innovation in Product Offerings: There is potential for innovation in developing new food intolerance products that meet consumers’ dietary needs without compromising on taste or texture, creating competitive advantages.

- Online Retail Expansion: The rise of e-commerce provides a platform for food intolerance brands to reach a broader audience, especially in regions with limited availability of specialty products in physical stores.

- Regional Market Expansion: There is a considerable opportunity to introduce food intolerance products into emerging markets, where awareness of such dietary needs is growing.

- Clean Labeling Demand: Increasing consumer demand for transparency in ingredients opens opportunities for brands to develop products with clean labels, free from additives and preservatives.

- Strategic Partnerships and Mergers: Collaborations with other industry leaders or health-focused companies can boost market presence and product development for food intolerance brands.

- Customization and Personalization: Offering personalized food intolerance solutions, such as tailored diet plans or subscription-based services, can attract health-conscious consumers.

- Government Initiatives: Government policies promoting health and wellness, including labeling regulations for food products, create a favorable environment for growth in the food intolerance segment.

RECENT STRATEGIES & DEVELOPMENTS IN THE MARKET

Product Launches and Expansions

- Data Point: In February 2023, Life Health Foods Pvt. Ltd. launched a new vegan drink, So Good Oat unsweetened beverage.

- Details: This dairy-free, plant-based milk alternative caters to the growing demand for plant-based drinks, suitable for use in tea, coffee, baking, and smoothies.

Strategic Partnerships

- Data Point: In October 2022, Beyond Meat partnered with Allana Group’s consumer products to introduce plant-based meat in India.

- Details: Beyond Meat aimed to expand its reach into over 25 cities in India, including Delhi, Bengaluru, Mumbai, Chennai, Kolkata, and Hyderabad, capitalizing on the rise of plant-based diets in India.

New Product Innovations

- Data Point: In May 2022, Danone launched Nextmilk, a dairy-free beverage under the Silk Canada brand.

- Details: The product was designed with a flavor profile and texture to appeal to dairy lovers seeking plant-based alternatives, solidifying Danone’s position as a leader in plant-based beverages.

Geographical Expansion

- Data Point: General Mills, Inc. focused on expanding its gluten-free and lactose-free product lines in emerging markets.

- Details: The company extended its product offerings in regions like Asia-Pacific and South America, where demand for food intolerance products is growing rapidly.

Acquisitions and Mergers

- Data Point: In 2023, Reckitt Benckiser Group PLC acquired a leading plant-based health brand.

- Details: This acquisition strengthens Reckitt’s position in the food intolerance market, particularly in the plant-based food sector, enhancing its product portfolio and market share.

Clean Labeling Trends

- Data Point: In January 2023, Califia Farms launched organic almond and oat milk with simple ingredients like purified water, sea salt, and almonds.

- Details: This product emphasizes clean labeling by excluding added oils or gums, aligning with the growing consumer demand for transparency in food ingredients.

Sustainability Initiatives

- Data Point: Nestlé SA has made significant strides in sustainability within its food intolerance product offerings.

- Details: The company is focusing on reducing carbon footprints and promoting environmentally friendly packaging for its plant-based and allergen-free products, reflecting the increasing trend toward sustainability in the food industry.

KEY BENEFITS FOR STAKEHOLDERS

Enhanced Market Insights

- Data Point: Stakeholders gain access to detailed market segmentation and trends analysis, which helps identify lucrative opportunities in the food intolerance products sector.

- Details: This enables better strategic decisions, market positioning, and resource allocation based on current and future market dynamics.

Increased Investment Opportunities

- Data Point: Growing consumer interest in health-conscious and clean-label products presents investment opportunities in emerging markets.

- Details: Stakeholders can invest in companies that are expanding their product lines or entering new markets, particularly in regions like Asia-Pacific and South America.

Improved Product Development

- Data Point: The increasing demand for innovative, allergen-free food products encourages R&D activities.

- Details: Stakeholders can benefit from the development of new products tailored to meet specific dietary needs, such as lactose-free, gluten-free, or vegan options.

Strategic Partnerships and Alliances

- Data Point: Collaborations like Beyond Meat’s partnership with Allana Group demonstrate the importance of forming alliances to expand market reach.

- Details: Stakeholders can leverage such partnerships to access new customer bases and enhance their competitive edge in the market.

Market Expansion Potential

- Data Point: Companies expanding their product portfolios in emerging markets benefit from increased market share and revenue.

- Details: Stakeholders involved in global expansions, such as Danone’s efforts in Canada, can take advantage of regional growth trends, particularly in Asia and South America.

Sustainability Leadership

- Data Point: Companies investing in sustainability, such as Nestlé’s initiatives in sustainable packaging, appeal to eco-conscious consumers.

- Details: Stakeholders can capitalize on the growing trend of eco-friendly and sustainable food products to boost brand loyalty and customer retention.

Enhanced Brand Equity

- Data Point: Clean labeling and product transparency, as seen with Califia Farms’ simple ingredient list, contribute to enhanced brand reputation.

- Details: Stakeholders can build trust and consumer loyalty by aligning with market trends for transparency and simplicity in food ingredients.

At DigiRoads Research, we emphasize reliability by employing robust market estimation and data validation methodologies. Our insights are further enhanced by our proprietary data forecasting model, which projects market growth trends up to 2030. This forward-thinking approach ensures our analysis not only captures the current market landscape but also anticipates future developments, equipping stakeholders with actionable foresight.

We go a step further by offering an exhaustive set of regional and country-level data points, supplemented by over 60 detailed charts at no additional cost. This commitment to transparency and accessibility allows stakeholders to gain a deep understanding of the industry’s structural and operational dynamics. By providing exclusive and hard-to-access data, DigiRoads Research empowers businesses to make informed strategic decisions with confidence.

In essence, our methodology and data delivery foster a collaborative and data-driven decision-making environment, enabling businesses to navigate industry challenges and capitalize on opportunities effectively.

Contact Us For More Inquiry.

Table of Contents

-

INTRODUCTION

- Market Overview

- Years Considered for Study

- Market Segmentation

- Study Assumptions and Definitions

- Market Scope

-

RESEARCH METHODOLOGY

-

MARKET OUTLOOK

- Executive Summary

- Market Snapshot

- Market Segments

- Product Type:

- Bakery Products, Confectionery Products, Dairy and Dairy Alternatives, Meat and Seafood, Sauces, Condiments and Dressings, Other Product Types

- Distribution Channel:

- Supermarkets/Hypermarkets, Convenience/Grocery Stores, Online Retail Stores, Other Distribution Channels

- Geography:

- North America (United States, Canada, Mexico, Rest of North America), Europe (Spain, United Kingdom, Germany, France, Italy, Russia, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, Rest of Asia-Pacific), South America (Brazil, Argentina, Rest of South America), Middle East and Africa (South Africa, United Arab Emirates, Rest of Middle East and Africa)

- Product Type:

-

COMPETITIVE LANDSCAPE

- Recent Strategies (Key Strategic Moves)

- Market Share Analysis

- Company Profiles

- General Mills Inc.

- Danone SA

- Beyond Meat

- Nestlé SA

- Reckitt Benckiser Group PLC

- Blue Diamond Growers

- Abbott Laboratories

- The Kellogg Company

- Oatly Group AB

- Dr. Schär AG/SPA

-

MARKET DYNAMICS

- Market Drivers

- Market Challenges

- Market Opportunities

- Porter’s Five Forces’ Analysis

- Bargaining Power of Suppliers

- Bargaining Power of Buyers

- Threat of New Entrant

- Threat of Substitutes

- Competitive Rivalry

-

GLOSSARY OF PROMINENT SECONDARY SOURCES

-

DISCLAIMER

-

ABOUT US